What Is Modified Duration?

Advertisement

Jan 16, 2026 By Rick Novak

Do you want to know what modified duration is and how it can impact your investments? Modified duration is an important measure of interest rate sensitivity that provides investors valuable insight into the risk associated with their investments.

It enables them to understand how effectively they manage investment risks by considering potential movements in bond yields over a given time frame.

In this blog post, we'll explore what modified duration is, why it matters for investors, and discuss a few tips on applying this helpful metric to make informed decisions about your portfolio. Read on to find out more!

What Is Modified Duration, and Why Is It Important To Know For Investors And Financial Professionals

Modified duration is a measure of interest rate sensitivity that helps investors and financial advisors understand the risks associated with their investments. It measures how much a bond's price will change when interest rates change.

A higher modified duration indicates that an investment is more sensitive to interest rate changes, while a lower modified duration suggests that an investment is less sensitive to interest rate changes.

Measuring and understanding the risks associated with an investment is essential for making informed decisions about your portfolio.

For example, suppose you have a bond portfolio with a highly modified duration. In that case, you should adjust your risk profile by introducing more diversification or hedging strategies to limit potential losses.

Understanding modified duration can also help investors identify opportunities to capitalize on changes in interest rates. Suppose you have a bond portfolio that has a low modified duration. In that case, consider investing in bonds when interest rates are expected to increase, as they will not lose value as quickly as high-duration investments.

By understanding and applying modified duration to your investment decisions, you can make more informed choices that will help ensure the success of your portfolio.

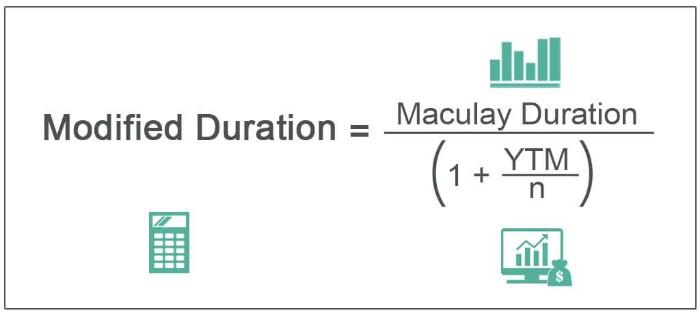

How To Calculate Modified Duration

Modified Duration measures a bond's sensitivity to changes in interest rates. It is calculated by taking the Macaulay duration, which measures a bond's price sensitivity to yield changes, and dividing it by one plus the current yield. This calculation provides investors with an indication of how much a bond's price will change when its yields fluctuate.

The formula for calculating Modified Duration looks like this.

Modified Duration = (Macaulay Duration / (1 + Current Yield)) x 100

Understanding modified duration can help investors better evaluate their portfolios over longer time frames. By considering potential movements in bond yields, investors can calculate how vulnerable their investments may be to interest rate changes.

For example, a bond with a high modified duration will experience more dramatic price fluctuations than one with a lower modified duration when the same change in interest rates is observed. By proactively evaluating the risk associated with their investments, investors can better manage potential losses or gains due to changing economic landscapes.

Finally, investors need to remember that Modified Duration is just one tool for assessing investment risks and should not be used as a substitute for comprehensive financial advice. To effectively manage your investments and minimize unwanted surprises, seeking professional counsel is always wise.

The Impact Of Changes In Interest Rates On Modified Duration

Modified duration is a measure of sensitivity to changes in interest rates. It indicates how the price of a bond, or an investment portfolio, will respond to changes in yield over time. The higher the modified duration of an investment, the greater its sensitivity to changes in interest rates. This means that when yields fall, prices rise and vice versa.

For example, if a bond has a modified duration of three years, the price of that bond would increase by 3% if its yield fell by 1%.

Similarly, the price of that same bond would decrease by 3% if yields rose by 1%. It's important to remember that since interest rates move both ways (up and down), the modified duration can be used to gauge both the potential reward and risk associated with an investment.

Ultimately, modified duration is a useful tool for investors that helps them understand the potential impact of changes in interest rates on their investments over time.

Importance Of Convexity When It Comes To Modified Duration

Convexity refers to the degree of curvature present in a bond's price yield curve. In other words, it's how much the price of a bond changes for every small change in its yield.

Investors often overlook the importance of convexity, but understanding how it affects modified duration can help investors better evaluate their investments. Convexity helps to capture the second-order effects on an investment's interest rate sensitivity that are not accounted for when calculating modified duration.

For example, if two bonds have similar maturities and coupon rates, but one has more convexity than the other, it will be less sensitive to yields because its price moves less with each change in yield.

Knowing this information can help investors decide which security is better suited to their portfolio.

Practical Applications Of Modified Duration In The Real World

In practical terms, investors can use modified duration to help determine how much they should expect an investment (or a portfolio) to change when bond yields change.

For example, suppose an investor holds a portfolio of bonds with various maturities, and the market experiences an unexpected increase in interest rates. In that case, the value of their bonds will decrease. Knowing the modified duration of their portfolio would give them insight into how much the value of their holdings could be expected to decrease in such a situation, which would help inform decisions about whether adjustments should be made.

In addition, the modified duration can also be used to compare different bonds or portfolios with similar characteristics. This allows investors to identify which investment has the least exposure to potential fluctuations in interest rates and therefore is likely to offer greater stability over time.

Common Mistakes To Avoid When Calculating And Using Modified Duration

Not considering embedded options.

Investors should always consider any embedded options in their calculations of modified duration, as these can significantly impact the results. For example, suppose a bond includes a call option. In that case, its effective life will be shorter than its stated maturity date, which must be considered when calculating modified duration.

Not accounting for cash flows.

Modified duration calculation focuses primarily on coupon payments; however, investors should also consider other cash flows that could affect their returns, such as principal or prepayment that could occur over the bond's life.

Focusing solely on modified duration

While modified duration can be useful in assessing risk, it does not tell the full story and should be used with other metrics. For example, investing in bonds with similar durations may not necessarily reduce the overall risk level if their yields and cash flows vary significantly.

FAQs

What is the modified duration of 1?

The modified duration of 1 equals the present value of a bond's cash flows discounted at its current yield.

What is the difference between Macaulay and modified duration?

Macaulay duration measures the weighted average term of a bond's cash flows, while modified duration indicates a bond's price sensitivity to changes in interest rates. Modified duration is calculated by dividing Macaulay duration with (1 + yield/m).

What are the risks associated with modified duration?

The main risk associated with modified duration is the potential for losses if interest rates change. Since bonds are sensitive to changes in yields, any increase or decrease in rates can cause a corresponding decrease or increase in the value of your investment. It's important to factor this into your decision-making when investing in bonds as part of your portfolio.

Conclusion

Modified Duration is an important concept for investors and financial professionals to understand, as the changes in interest rates can significantly impact the value of a bond. It is also important to be aware of convexity and its relationship to modified duration, as this can profoundly affect the stability and risk associated with certain investments. Lastly, if you need help with how calculating or using modified duration in your financial endeavors, it is always best to seek professional advice.

On this page

What Is Modified Duration, and Why Is It Important To Know For Investors And Financial Professionals How To Calculate Modified Duration The formula for calculating Modified Duration looks like this. The Impact Of Changes In Interest Rates On Modified Duration Importance Of Convexity When It Comes To Modified Duration Practical Applications Of Modified Duration In The Real World Common Mistakes To Avoid When Calculating And Using Modified Duration Not considering embedded options. Not accounting for cash flows. Focusing solely on modified duration FAQs What is the modified duration of 1? What is the difference between Macaulay and modified duration? What are the risks associated with modified duration? ConclusionAdvertisement

What Exactly Is Trading Before And After The Market Opens

Rules from the World's Top Investors

Bank Account to Help Raise Your Credit Score

Varieties of Investments In Portfolios

The Difference Between Payday and Installment Loans

What Is a Value Fund?

Knowing your Available Credit and Credit Limit

InCharge Debt Solutions Review